Valvest Anlagegrundsätze

Oct 29, 2024Investing On Valvest

The Spanish real estate market continued its solid expansion through the third quarter of 2025, extending the strong upward trajectory seen earlier in the year. Spain’s climate, coastal lifestyle, and overall quality of life continue to attract both domestic and international buyers.

Recent data confirms that housing prices rose notably again in Q3 2025, a clear signal that market confidence remains high. For investors, second-home seekers, or those considering relocation, this period offers a favorable entry point into a resilient and maturing property market.

In this report, we explore the main Q3 2025 property trends, city-level developments, and the challenges and opportunities shaping the coming months.

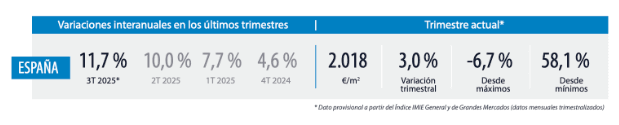

National Overview

According to Tinsa’s Local Markets Report (Q3 2025), the average price of completed homes (new and resale) in Spain rose +11.7% year-on-year and +3.0% quarter-on-quarter. Adjusted for inflation, this equals real growth of 8.6%, confirming the Spanish housing market’s continued upward trajectory.

Residential demand remains robust, supported by steady employment, improved consumer confidence, and lower mortgage costs. Home transactions increased +7.6% year-to-date, while mortgage originations rose +18.7% according to Notaries (and up to +38.3% per INE), reflecting strong buyer confidence.

The rental market remains under structural pressure, with supply lagging demand. This imbalance keeps rental yields attractive, particularly in high-demand urban and coastal areas.

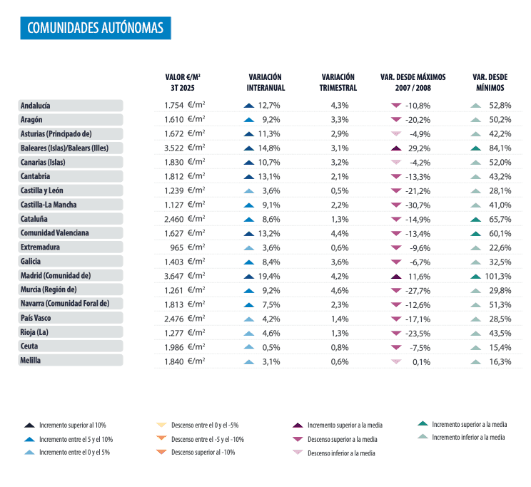

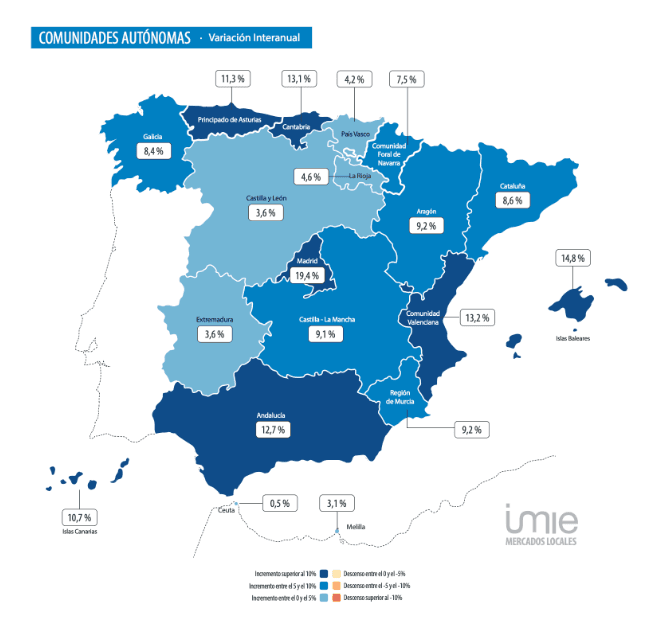

Performance by Autonomous Community

In Q3 2025, residential prices in Spain continue to rise, with Madrid, Balearic Islands, and Valencian Community leading the growth:

Quarterly changes in these regions ranged between +0.5% and +4.6%, showing steady momentum without contractions.

Overall, real estate investing in Spain remains attractive thanks to sustained demand, limited supply, and favorable financing conditions.

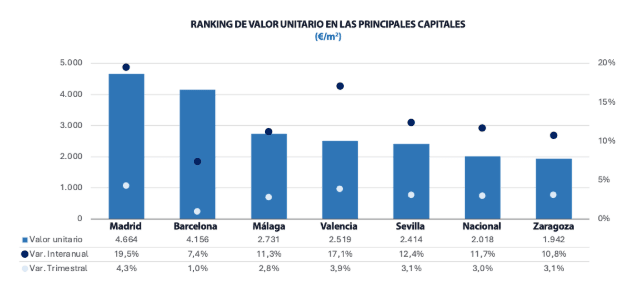

Development in Major Cities

Spain’s capital cities often lead market cycles, showing sharper price changes and revealing underlying demand and affordability pressures across regions.

Seven cities, including Madrid, Valencia, Málaga, and Palma, have now surpassed their 2007 price peaks, underscoring the resilience of the Spanish property market.

Regulatory and Legal Changes In Q3 2025, Spain introduced tighter regulations on property management and short-term rentals (Tinsa, 2025). The Single Register for Short-Term Rentals became mandatory, while reforms to the Horizontal Property Law allow owners’ associations to limit tourist rentals. Fiscal measures, such as taxes on vacant homes and adjustments for large property holders, are under discussion. These changes affect both national and regional markets, including Valencia, aiming to balance tourism demand with housing affordability.

Interest Rates and Mortgage Access Falling interest rates in early 2025 reduced mortgage costs, supporting strong demand (Tinsa, 2025; Banco de España). Mortgage-financed sales accounted for ~53% of total transactions in Q3, with the national average loan-to-value ratio at 65%. Theoretical debt service ratios indicate that some urban areas, including Madrid, Málaga, Barcelona, Sevilla, and Valencia, require households to allocate 45–56% of their income to mortgage payments if purchasing a standard property. Future rate increases could reduce affordability and slow transaction volumes.

Growing demand in secondary cities

Beyond Madrid and Barcelona, secondary cities such as Valencia, Seville, and Málaga are experiencing strong price growth and high buyer interest. Valencia, in particular, has seen residential prices rise +13.2% year-on-year, reflecting increasing popularity among domestic and international buyers. These cities offer entry points for real estate investment in Spain with strong rental yields.

Long-term rental market expansion

The long-term rental segment remains robust, driven by structural supply constraints and rising property prices. Rental demand continues to outpace availability in urban centers, keeping yields attractive. Investors focusing on stable, long-term rental income can benefit, especially in dynamic cities where population growth and urbanization are strong.

This trend is clearly visible in Valencia, where local and international tenants increasingly seek high-quality, professionally managed housing. At Landed, our own portfolio of short-stay and mid-term rental apartments reflects this ongoing demand — maintaining consistently high occupancy and above-expected performance throughout Q3 2025.

One of Landed’s managed short-stay apartments in Valencia, reflecting the city’s strong rental demand and investment performance.

One of Landed’s managed short-stay apartments in Valencia, reflecting the city’s strong rental demand and investment performance.

Digital nomad influx and mid-term rentals

Remote work and the growth of digital nomad communities are creating new opportunities in mid-term rentals, typically ranging from one to twelve months. Coastal cities with good infrastructure, such as Valencia, Barcelona, and Málaga, are becoming popular among international remote workers. Properties adapted for flexible leasing can achieve higher returns than conventional rentals.

Renovation and value-add potential

Older housing stock in urban cores presents opportunities for renovation and value-add strategies. Upgrading apartments and buildings to meet modern standards can significantly increase rental income and resale value. This approach is particularly effective in cities where supply is limited but demand remains strong.

The Spanish real estate market showed robust growth in Q3 2025, with strong price increases in Madrid, Barcelona, Valencia, and other secondary cities. Rising demand, limited housing supply, and structural rental constraints are driving both capital appreciation and attractive rental yields. Opportunities exist across segments: long-term rentals, mid-term stays, and renovation projects. Coastal and high-demand cities offer stable returns, while secondary cities provide strong growth potential. Strategic positioning requires monitoring interest rates, regulatory changes, and housing supply. Spain remains a favorable environment for property investment through the remainder of 2025, with robust returns supported by ongoing Q3 2025 property trends and high buyer confidence.